FangQuant › Daily Morning

Introduction to China A50 Interconnection Index Futures of HKEx

[Introduction to China A50 Connectivity Index Futures of HKEx] MSCI China A50 Connectivity Index Futures is expected to enrich the 50 product system, and the listing of new products will bring a lot of allocation/hedging requirements.

Key points of the report: MSCI China A50 Interconnection Index Futures is expected to enrich the 50 product system, and the listing of new products will bring a lot of allocation/hedging demand.

Summary

Event: August 20, 2021, HKEx announced that it has entered into a new authorization agreement with MSCI to launch futures contracts with the MSCI China A50 Interconnection Index in October 2021.

Characteristics of MSCI China A50 Index:

1) The correlation coefficients of MSCI China A50 Index (Bloomberg dimension), SSE 50 and FTSE A50 are 0.979 and 0.993 respectively, which can be regarded as the approximate substitution of SSE 50;

2) from January 2011 to June 2021, MSCI China A50 index of the annual return of up to 8.3%, slightly higher than the SSE 50 5.3%, FTSE A50 of 6.0%.

Detailed Rules for Futures Contracts: The design of MSCI China A50 Interconnection Index Futures is similar to that of Singapore FTSE A50 Futures: 1) Both are priced in USD; 2) the main trading sessions are concentrated on 09:00-16:30; 3) the listing contracts are all 6; 4) the last trading day is slightly different, the former is Friday, the third week of the contract month, the latter is the penultimate trading day of the contract month. MSCI China A50 Interconnection Index Futures is expected to enrich the 50 futures product system and provide more choices for overseas funds.

Potential investment groups: 1) Passive index funds tracking of MSCI. Assuming that the inclusion factor rises from 20% to 50%, the size of global passive funds tracking A-shares is expected to rise to 383.5 billion, and if there are 3% passive funds to choose futures allocation, the corresponding capital size will 11.5 billion; 2) The active influx of foreign capital after the inclusion of MSCI. Drawing on the experience of Taiwan China after its inclusion in MSCI, the trading volume of foreign and inland participating futures increased at an annualized 36% rate from 1998 to 2006. Assuming that the growth rate of foreign capital in domestic stock index futures is similar until 2025, it is estimated that the potential position of foreign capital in domestic stock index can reach 240 billion. If the proportion of MSCI futures position is 10% of the total amount, the corresponding allocation/hedging requirements are also 24 billion.

Risk Point: 1) The difference between MSCI China A50 Interconnection Index and Wind, Bloomberg is too large

Event: August 20, 2021, HKEx announced that it has entered into a new authorization agreement with MSCI to launch futures contracts with the MSCI China A50 Interconnection Index in October 2021.

I. Differences between MSCI China A50, SSE 50 and FTSE A50

(I) Weight and correlation

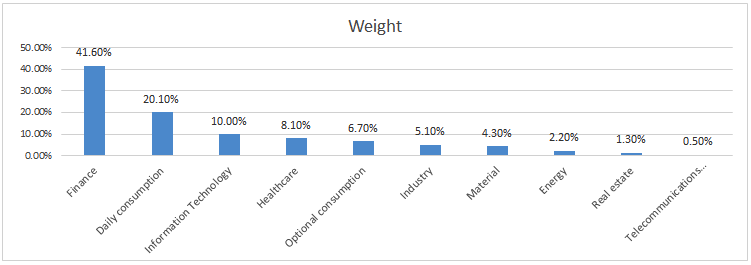

As the weight details of the MSCI China A50 Interconnection Index have not been disclosed by HKEx, this paper replaces the analysis with the MSCI China A50 Index (Bloomberg dimension). According to the weight dimension, the top three weight industries of MSCI China A50 Index are finance, daily consumption and information technology, accounting for 41.6%, 20.1% and 10.0% respectively. After 2011, the correlation coefficients of MSCI China A50 Index, SSE 50 and FTSE A50 are 0.979 and 0.993 respectively, and MSCI China A50 Index and SSE 50 can be approximately substituted.

(II) Statistical indicators

After statistical 2011, the statistical indicators of SSE 50, FTSE A50 and MSCI China A50(Bloomberg dimension) show that: 1) the Sharpe dimension, MSCI China A50 is the highest and can reach 0.146; 2) The high Sharpe is related to its annualized return, and the annualized return of MSCI China A50 can reach 8.3%, slightly higher than SSE 50(5.3%) and FTSE A50(6.0%);3) the volatility dimension, the annualized volatility of the MSCI China A50 can reach 22.8%, which is comparable to the SSE 50 and the FTSE A50.

II. Introduction to futures contracts and potential investment groups

(I) Contract Rules

In terms of contracts, the design of MSCI China A50 Interconnection Index Futures and Singapore FTSE A50 Futures have many similarities: 1) Both are priced in US dollars; 2) the main trading sessions are concentrated in 09:00-16:30;3) There are 6 listed contracts; 4) There is a slight difference in the last trading day, where the former is Friday of the third week of the contract month and the latter is the penultimate trading day of the contract month. MSCI China A50 Interconnection Index Futures is expected to enrich the 50 futures product system and provide more choices for overseas funds.

|

Futures contract comparison |

SSE 50 Index Futures |

HSCI China A50 Connectivity Index Futures |

Singapore FTSE A50 Futures |

|

Transaction currency |

Renminbi |

Dollar |

Dollar |

|

Contract multiplier |

300 RMB/point |

USD 25/point |

USD 1/point |

|

Tick Size |

0.2 point |

0.2 point |

1 point |

|

Contract month |

The current month, the next month and the next two quarterly months |

The current month, the next month and the next four quarter months |

Two recent monthly contracts and March, June, September, and December of the 1-year cycle |

|

transaction hour |

9:30-11:30; 13:00-15:00 |

09:00-16:30; 17:15-03:00 |

09:00-16:30;17:00-05:15 |

|

Time of last trading day |

9:30-11:30; 13:00-15:00 |

09:00-15:00; |

09:00-16:30 |

|

Last trading day |

Friday of the third week of the contract month |

Friday of the third week of the contract month |

The penultimate trading day of the contract month |

(II) Main participants in futures

A. Index funds

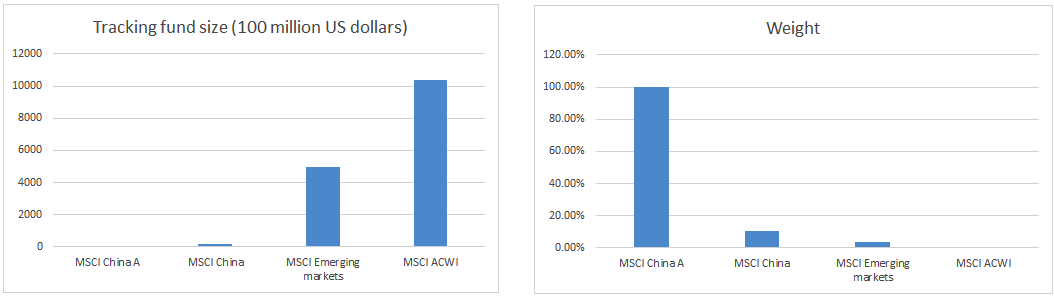

The first category of funds is index funds that track MSCI. According to Bloomberg data, the current volume of funds for passive tracking MSCI ACWI, MSCI Emerging Markets, MSCI China, and MSCIChinaA is 1036.2 billion, 499.2 billion, 15.96 billion, and USD 3.63 billion, respectively, based on the 20% inclusion factor, it is estimated that the weight of A shares in MSCI ACWI, MSCI emerging markets and MSCI China is 10.6%, 3.4% and 0.4% respectively, and the amount of capital corresponding to A shares tracked is USD 26.9 billion, which is converted at the 6.5 exchange rate, the corresponding market value of RMB is about 175 billion. If the subsequent inclusion factor is gradually raised to 50%, the corresponding weight of A shares in MSCI ACWI, MSCI emerging markets and MSCI China will be raised to 1.1%, 8.1% and 22.9% respectively, the amount of funds corresponding to tracking A-shares rose to US $59 billion (RMB 383.5 billion). If the relevant MSCI futures are subsequently listed and allocated by futures at a 3% proportion, the market value of the futures of the MSCI fund can reach 11.5 billion.

B. Active influx of foreign capital after inclusion in MSCI

The second category of funds is the voluntary influx of foreign capital after the inclusion of MSCI. Combined with the experience of China Taiwan and South Korea in MSCI, the proportion of follow-up overseas investors will be continuously improved. In Taiwan, China, for example (1996 first included), the share of 1996 foreign investors was only 7.27%, But 2006 ten years later, the share rose to 22.19%. With the increase of the participation in the spot market, the participation in the futures market has also increased. 1998 the proportion of foreign capital and inland capital in futures trading is almost 0%, the proportion has soared to 9.29% in 2006, the compound annual growth rate of futures trading volume reached 36.6%.

In 2016 and 2017, the QFII stock index position data disclosed by China Futures Association in the interim agreement is 15318 lots and 18767 lots respectively, assuming that the holding contracts are IF contracts in the current month, the market value of the corresponding position is 15.1 billion and 22.7 billion (the turnover increased by 50% year-on-year). With reference to the data included in MSCI from Taiwan, assuming that QFII Holdings will grow at an annual growth rate of 36% until 2025, foreign holdings in the stock index can reach 240 billion. Assume that the market value of the MSCI futures position accounts for 10% of the total, and the allocation/hedging requirements for inclusion in MSCI are estimated for 24 billion.

III. Summary: The potential market for MSCI futures is broad

To sum up, the listing of MSCI China A50 index futures marks the formal entry of MSCI futures into investors' vision. With the accelerated opening of the domestic capital market, the subsequent potential market is broad.

Currently no Comments.

Hot Topics

The 13rd China International Future Forum

The Shanghai Derivatives Energy Forum has received extensive attention from relevant industries both within and outside the borders.

Financial institutions deep explore commodity market opportunities, commodity index financial products show full-scale trend

R-Code for analysis: getKDJ

New indicator to analyze the arbitrage opportunities between sse50 and csi500

R-Code@June 06, 2016

Market review: January 11, 2017

The Great China Bubble: Anniversary Lessons and Outlook

Quant Investment in China A-share market

The hedge strategy between SSE50 and A50--Jan 13,2017

The arbitraging strategy between CSI300 and SSE50

Market review: June 17, 2016

Sleepless in London--Enda Homan(Allied Irish Banks Plc)

MSCI Rebuffs Chinese Equities for Third Time in Blow to Xi

Soros, Druckenmiller among hedgies profiting in market plunge