FangQuant › Strategies

Strategy Update:

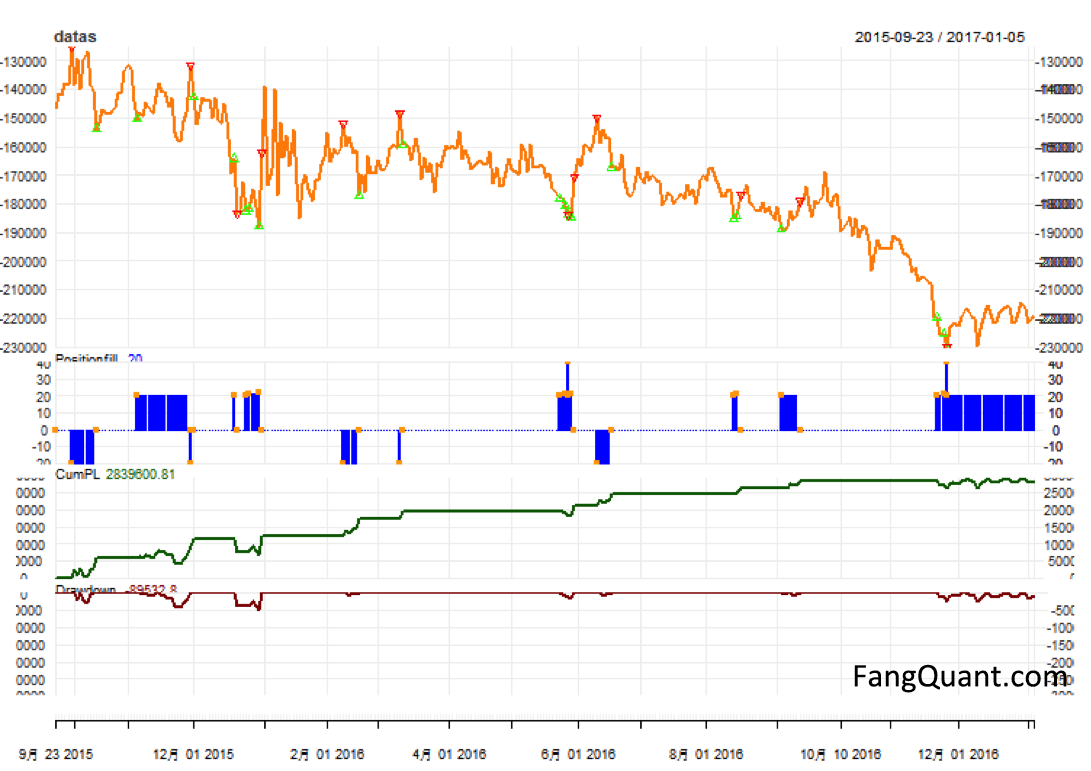

1) The latest run result as followed:

Last PL: 2910213 Biggest drawDown: -498050.6 Total buy(times): 15 Total sell(times): 5 Max Margin: 4434984 max buy position: 22 max sell position: -20 start money: 5e+06 Annual return: 0.4590242 Volatility: Max Max Drawdown(Ratio): 0.08078893

2) Strategy chart:

We observed that spread continued to widen between SSE50 and A50, probably due to tightness in China money market and the expectation of RMB devaluation, which made investors hesitate to long SSE50, so the SSE50 price showed increasing weakness against A50.

The newest hedging ratio between SSE50 and A50 is 1:13, instead of 1:14 in our report in October 2016.

As the picture above:

The yellow lines is the trend of difference (SSE50*300– 13*A50*USDCNY);

The green points mean SSE50 is under-valued, and we long SSE50,short A50.

The red points mean that SSE50 is over-valued, and we short SSE50, long A50.

The blue line below present the changing of the positions we build due to the strategy.( up one point means we long the spread one time, down one point means we short the spread one time)

The dark green and red lines below present the return and the maximum drawback of the strategy respectively.

The dates of buying and selling signal are listed below:

> rownames(as.data.frame(datas[datas$buy>0])) [1] "2015-11-05" "2015-12-18" "2015-12-24" "2015-12-25" "2015-12-30" "2016-05-24" [7] "2016-05-26" "2016-05-27" "2016-05-30" "2016-08-12" "2016-08-15" "2016-09-02" [13] "2016-11-22" "2016-11-24" "2016-11-25"

To be more specific, the buying signals after October 2016 are listed below:

> buys[buys>as.Date('2016-10-01')]

[1] "2016-11-22" "2016-11-24" "2016-11-25"

3) Strategy review:

We adopted the widely used mean-reversion strategy to generate signal for the SSE50-A50 Spread Trading system.

The daily residual from fitting A50 on SSE50, named “e”, is treated as “stock price”, to calculate the moving average. A large deviation from the average meant there’s trading opportunity.

We regressed A50 on SSE50 with the first 50 daily close prices, with the R code below, and get the first e.

for(i in (L+1):num_all){

lm1<-lm(y_all[1:(i-1)]~x_all[1:(i-1)])

e_all[i]<-y_all[i]-lm1$coefficients[[2]]*x_all[i]-lm1$coefficients[[1]]

}

For the moving average of e we used 30-day mean, as in R code below:

mas[i]<-mean(past_prices) sigmas[i]<-sd(past_prices)

Lastly, the newest e is compared to moving average of e and calculated the deviation.

daily_sigma[i] = (current_price - mas[i]) / sigmas[i]

The times of deviation over sigma is also calculated as a measure of winning probability, as R code below.

for(sig in minp:(maxp-w-1)){

wls<-my_data[my_data$pvs>=sig&my_data$pvs<(sig+w),2]

ratio=sum(wls=="win")/length(wls)

if(length(wls)/total >= least_percentage){

if(best_ratio<ratio){

best_ratio<-ratio

lower<-sig

uper<-sig+w

}

}

}

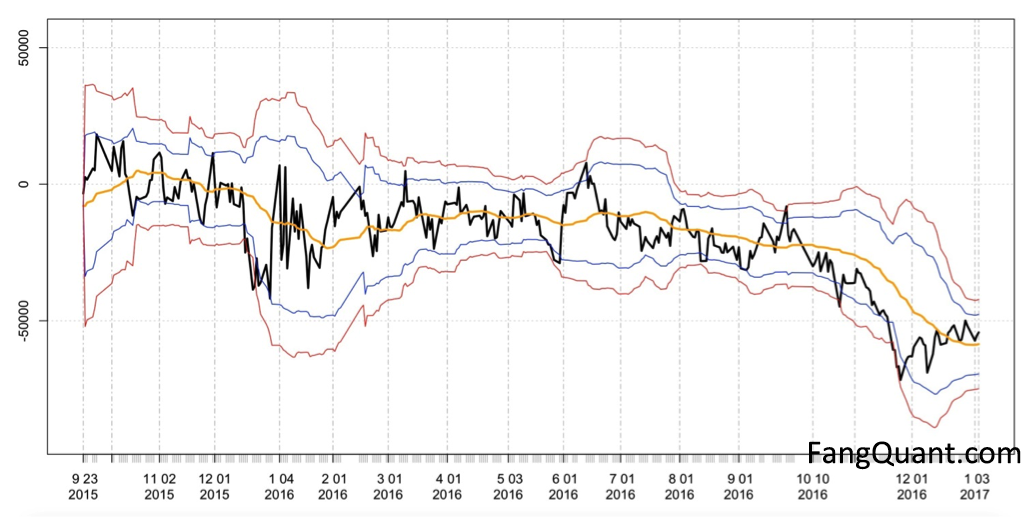

4) The graph showed the residual e of A50 fitting with SSE50 and upper and lower bounds of sigmas.

The black line is the trend of daily residual e;

The yellow line is the trend of daily average MA;

The red and blue lines are the trend of upper and lower bounds which calculated according to the deviation ρ and volatility σ.

Currently no Comments.

Hot Topics

The 13rd China International Future Forum

The Shanghai Derivatives Energy Forum has received extensive attention from relevant industries both within and outside the borders.

Financial institutions deep explore commodity market opportunities, commodity index financial products show full-scale trend

R-Code for analysis: getKDJ

New indicator to analyze the arbitrage opportunities between sse50 and csi500

R-Code@June 06, 2016

Market review: January 11, 2017

The Great China Bubble: Anniversary Lessons and Outlook

Quant Investment in China A-share market

The hedge strategy between SSE50 and A50--Jan 13,2017

The arbitraging strategy between CSI300 and SSE50

Market review: June 17, 2016

Sleepless in London--Enda Homan(Allied Irish Banks Plc)

MSCI Rebuffs Chinese Equities for Third Time in Blow to Xi

Soros, Druckenmiller among hedgies profiting in market plunge